Trilogy: The First Financial Problem Families Face After a Death

March 16, 20265 min read

Not grief. Information. Or the lack thereof.

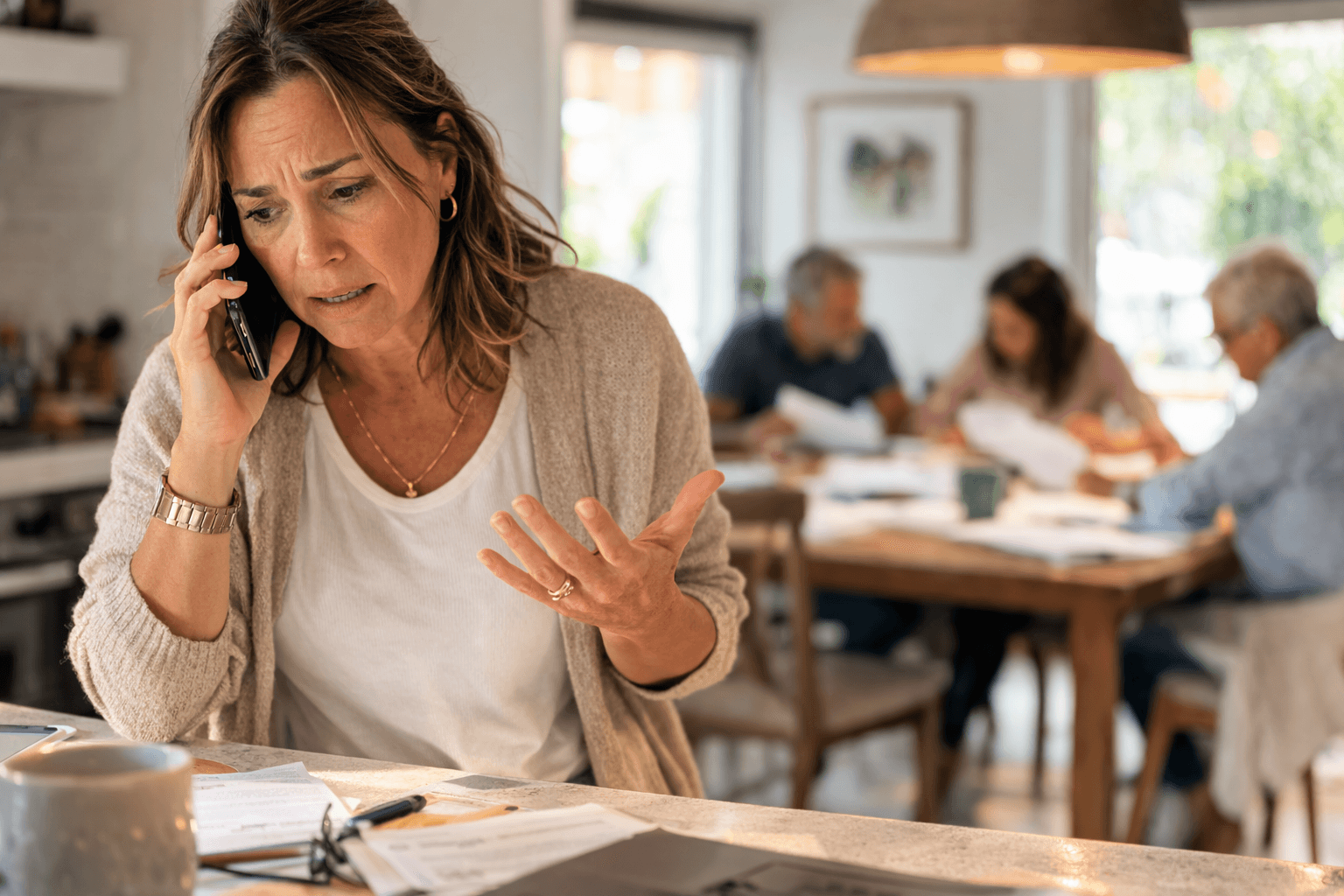

There is a moment that happens in many families within the first few days after someone dies.

Someone sits down to figure out what needs to be done next.

They open a laptop, gather mail from the kitchen counter, and start asking simple questions.

Where are the bank accounts?

What investment firms are involved?

Is there life insurance?

Who is the financial advisor?

What bills are due this month?

And very quickly another realization follows.

No one knows the full picture.

Not completely.

Not with certainty.

This is the first operational challenge many families encounter after a death.

It is not the legal process.

It is information.

The common assumption

Most people believe that when the time comes, the details of their financial life will be easy to find.

They imagine there is some central place where everything exists. A folder in a filing cabinet. A spreadsheet on a computer. A document labeled "important information."

But modern financial lives rarely work this way.

Instead, information tends to exist in fragments. Some of it lives in a person's memory. Some of it lives in email. Some of it is stored on a laptop or phone. Some of it exists only as statements arriving in the mail.

In many households, no single person has ever seen the entire picture at once.

The frantic search

Executors and family members often begin by trying to identify basic financial facts.

Where are the accounts?

What institutions are involved?

What insurance policies exist?

What credit cards are active?

What subscriptions or loans exist?

Clues appear gradually.

A statement arrives in the mail. A tax return reveals the name of an investment firm. An email inbox contains a confirmation from an insurance company. A contact stored in a phone identifies a financial advisor.

Piece by piece, the picture begins to form.

But rarely all at once.

Why modern financial lives make discovery difficult

Over the course of a lifetime, most adults accumulate financial relationships across many institutions.

Accounts are opened when someone starts their career, changes banks, moves cities, joins an employer retirement plan, purchases insurance, or begins investing through a new platform. Many of those accounts remain open for years or decades.

Studies of household financial behavior consistently show that a typical adult maintains financial relationships with 10 to 20 different institutions over their lifetime.

Those relationships often include:

- banks and credit unions

- investment firms or brokerages

- employer retirement plans

- insurance providers

- credit card issuers

- government benefit programs

- digital financial platforms

Each institution holds only a small piece of the picture.

Unless someone has intentionally documented where everything lives, families must discover those pieces one by one.

The hidden work of estate administration

Much of the early work of administering an estate involves simply identifying what exists.

Executors must locate assets before they can administer them. Insurance policies must be found before claims can be made. Financial institutions must be identified before accounts can be transferred or closed.

Even basic tax reporting requires a complete inventory of income sources and assets.

When information is scattered or incomplete, this discovery phase can take weeks or months. Executors spend time searching through email accounts, contacting institutions, reviewing past tax returns, and speaking with advisors in an attempt to reconstruct the financial picture.

Assembling the needed information is one of the most time-consuming parts of the entire process.

Why a Will alone does not solve this problem

A Will answers important legal questions.

It appoints the executor and establishes who inherits the estate.

But most Wills do not contain a detailed inventory of accounts, policies, and obligations. The document defines authority and distribution, not the operational details of someone's financial life.

Even when the legal structure is clear, the executor still needs to locate the assets and identify the institutions involved.

Without organized information, families can spend months reconstructing something that could have been documented in minutes.

Information readiness makes all the difference

Information readiness means the people who may one day need to step in know where to start.

At minimum, they can identify:

- where financial accounts are held

- what insurance policies exist

- who the key advisors are

- where important documents are stored

- what obligations must continue to be paid

When that information is organized and accessible, the early stages of estate administration look very different.

Instead of reconstructing a financial life, executors can act with clarity and confidence.

Estate readiness requires more than legal documents

Legal readiness determines who has authority.

Information readiness determines whether they can actually act.

Both matter.

Because when the time comes, the hardest part of managing an estate is often not the law.

It is finding the information that makes action possible.

This article is part of a three-piece series illustrating the three Estate Readiness pitfalls

See also: What Happens to Your Bank Accounts When You Die and The Hardest Questions Families Face Are the Ones No One Explained